There are two sides to a credit card transaction; Authorization and Settlement. Between these two stages of the transaction process there are 4 basic functions to all credit card terminals. In this write up we are going to go over both sides of the transaction and each of the basic functions in detail. While this is going to be a highly simplified explanation it should be more than enough to firmly grasp the concepts and proper use of a standard credit card terminal.

Sale:

Running a sale on a terminal initiates the authorization side of the transaction. This is when the terminal communicates and makes the approval request. If that request is approved the terminal will receive an approval code from the issuer and the transaction is stored in the terminal until the settlement is processed. At this point the transaction has only been authorized and no money has been moved and you are still able to alter the transactions.

Don’t confuse the Sale function with functions like Authorization Only. While auth only is outside the scope of this writing, it is not the same as a sale.

Settlement:

The settlement process finalizes all transactions processed on the terminal. This is the point when funds begin to move, discount rates are charged, and you are no longer able to alter transactions.

Transaction manipulation for most businesses refers to the voiding which we will get into shortly. Still other businesses like restaurants or lodging may utilize tipping or check-in check-out functions. You can only manipulate a transaction before it has settled.

If your terminal is set to automatically settle each day it is a good idea to review your settlement report to make sure it shows the batch settled successfully. It’s ultimately the merchant’s responsibility to verify that the terminal is settling.

Void:

A void is a type of refund that is done before a transaction is settled. When you void a transaction, it keeps the funds from moving, and therefore keeps the business from having to pay discount fees on the original sale. Voiding effectively just deletes the transaction from the settlement entirely. This results in the card holder seeing a pending transaction on their account for a few days before it eventually disappears.

There is also a function called a reversal which voids the sale and contacts the issuer requesting that the authorization or pending amount be released back to the card holder. For some devices this can be included as part of its batch function, for some it’s a separate function, and for others it’s not an option at all. If you have a reversal option on your terminal you should contact your processor for information about how to use it, as it’s a better customer experience.

Return:

If a transaction has already settled and you need to refund the card holder, your only option is going to be to perform a return. Unfortunately, that means funds will have already started moving and you are going to be charged your discount rate for having settled the sale. You really shouldn’t be charged an additional percentage for the refund however, we have seen processors who did charge their merchants for returns as well. If your processor charges an additional discount for returns, then it’s probably a good time to look for other processing options.

It’s also important to note that it is extremely important that you refund card holders the same way they originally paid. For example, don’t give a cash refund to someone who paid you on a credit card. The reason is there is no paper trail for the refund. If the card holder contacts their issuer and disputes the original transaction, you cannot prove you refunded previously, and will most likely lose the dispute as well as the money you already paid. Also, if a customer pays cash you wouldn’t want to refund them on their credit card, as that could cause some risk related issues on your merchant account.

Conclusion:

There are many functions a standard credit card terminal can do. For most every merchant these are the only 4 you will ever use. If a customer or issuer ever tells you to use a function that is not listed here, you should immediately contact your processor and explain the situation and get support on whether you should do what they are asking. Card holders and issuers should not be trusted when it comes to how to process sales or refunds. Many times, they will be trying do something fraudulent, other times they could cause problems down the road for you just due to their lack of understand the functions they are asking you to use.

MasterCard has entered phase two of its Dispute Resolution Initiative (MDRI) and so we felt that now was a good time to shoot out some information about what has changed in the world of chargebacks and what changes are still on the horizon. But first some history…

While credit itself has been around about as long as the world’s oldest profession, it wasn’t until the 1950’s when Diners Club released the first credit card, for our modern system of credit issuing and acceptance to take form. In the mid 1970’s, chargebacks were introduced to help build consumer confidence in a time when many people were still wary about revolving credit accounts. Since then times have changed and the credit card along with them.

The credit card industry is in a constant state of change, but it requires deliberate effort to make those changes. The chargeback system is a part of the industry that has been largely neglected for the past 50 years, but a year ago that started to change.

In April 2018 Visa released its Visa Claims Resolution (VCR) initiative which was a major overhaul of its chargeback system. VCR was designed to stop fake or fraudulent chargebacks as well as streamline the entire chargeback process. Before VCR, the average chargeback resolution time-frame for Visa was a whopping 46 days, with some disputes continuing for more than 3 months. Visa’s new chargeback initiative has just turned one, and it’s still too soon to tell how it will mature, so far there have been mixed reviews at best.

Unlike Visa, MasterCard is rolling out its new system relatively slowly in 4 phases over 18+ months. Phase one started in Oct 2018 requiring issuers to collect more information from cardholders before allowing a chargeback for a number of reason codes. This additional information should help MasterCard weed out invalid disputes before they start attempting to limit outright fraud on the part of cardholders who issue deliberately false chargebacks, typically known as friendly fraud.

Phase 1 – Affected Reason Codes:

4831 – Incorrect Transaction Amount

4834 – Point of Interaction Error

4853 – Cardholder Dispute

4863 – Cardholder Does Not Recognize

Phase 2 is where we catch up to present day and effects how merchants handle chargebacks and refunds. Basically, if a business receives a chargeback under these new rules the business should not refund the original transaction. Instead the merchant should continue to work through the chargeback process and let that process handle the funds.

If a business receives a chargeback and later decides to refund the card holder, even after winning that chargeback, the issuer can still issue a second chargeback resulting in the business being out the money twice. While there is a way to contest the double debit it would be easier to just not have to deal with that in the first place.

This phase also shortens the filing time frame on reason code 4834 (Point of Interaction Error) from 120 day to 90. It also removes two reason codes all together.

Phase 2- Affected Reason Codes:

4834 – Point of Interaction Error – Chargeback time-frame lower form 120 to 90 days.

4840 – Fraudulent Processing of Transactions – Removed as a chargeback reason code.

4863 – Cardholder Does Not Recognize – Removed as a chargeback reason code.

Phase 3 is an unknown at this time. We know its scheduled to start in October 2019, however MasterCard has yet to state what exactly this phase is. We will post an update as we get more information about this phase and what to expect.

Jumping to April 2020 and beyond, phase 4 will stop allowing subsequent chargeback reason codes. Instead, issuers will be able to continue a dispute with pre-arbitration which is very similar to Visa’s new setup.

Only time will tell how effective these changes are at improving the chargeback system and minimizing bogus chargebacks. So far, just based on Visa’s VCR initiative, we wouldn’t expect too much, at least initially. It is promising to see both Visa and MasterCard taking steps in the right direction. However, it may take many years before we see any real improvement at the merchant level. Until then, we will move forward cautiously optimistic that associations are attempting to level the playing field and making the chargeback process more fair to merchants.

Regardless of your market accepting credit cards is just part of today’s world. Doing so can be an intimidating task for an uninformed business owner. Yet the process to accept payments does not have to be an arduous task. Following some simple steps and having a basic understanding of the credit card industry, any business owner can feel confident in choosing a payment provider.

First Step

The first step to accepting non cash payments, is to understand how the business will be accepting payments. Are they going to be using a counter top terminal or a point of sale systems? Are they going to be accepting sales over the phone, keying in the transactions, or online through an eCommerce store? It can even be a combination of these options. If the business is going to get quotes from providers, it’s best to know what they need or might need in the future. This allows the business to confirm upfront what it’s going to cost, and if it’s something the processors they are talking to are able to support.

Choosing a Payment Provider

Many business owners, when just opening their doors, first go to their bank to accept credit cards. This is not always the best option, as these banks typically have higher rates, less knowledge across the industry, and have a lack of personalized customer service.

The reason for this is pretty simple. Traditional banks specialize in savings and loans and payment processing is a value add that they offer. Since it’s only a side offering they do not dedicate their resources to it, and instead use a third party to handle the account setup and maintenance. In this case it’s the same as going through any other independent agent or merchant account sales organization. Generally banks and those third parties expect people coming directly through them are not likely shopping around much. Which is typically why they can get away with charging higher prices than the rest of the industry.

When choosing a provider, it can be extremely beneficial to find one that specifically deals in credit card processing and payment acceptance across various platforms. Specialized processors are able to provide competitive equipment pricing, competitive rate structures, and specific acumen for each individual business needs.

Choosing who to trust your business with, is the most important factor when entering the industry of credit card processing. It is important to do the research, and know the questions to ask.

How long have you been helping businesses accept credit cards?

Do you have a testimonials or references?

What is your primary website?

What kind of equipment/service would you suggest for my business?

What are your monthly fees and processing rates?

What kind of contracts do you offer?

How long will it take before I can start accepting payments?

While these are just a few pertinent questions, it is important to note the preparedness and sincerity of the feedback. The answers to these questions will help the business owner be able to compare between various processors, and make an educated decision on which company will provide the best option for the specific business needs.

In our next article we will go over several great questions to ask your processor and what answers you should expect.

Being prepared for the process of underwriting will drastically prevent the chances of any delays. Sometimes businesses need to get up in running as soon as possible, but run into issues with applications.

Applications departments typically run separately from the sales teams, and sometimes it would seem they do their best to block incoming applications. It is however their job to assess risk and prevent any sort of fraud or illegal business from accessing the payment network.

Business owners should be prepared to fill out the application completely, and return it complete with a voided check or bank letter. The business may also want to include the following as processors may request this information, especially for a new business.

Proof of Existence

Governmental filings: DBA, EIN , Business License

Marketing Docs: Promo Material, advertisements

Photos of business location inside and out.

Business Financials (less likely for most businesses)

1 to 3 years of complete financials

previous years tax return if financials are not audited

Industry Licences (if applicable)

If the underwriters have this information at hand when looking at a new account, it can really speed up the process. This also allows them to get a better understanding of the business and to confirm its legitimacy.

The underwriters will then take into account all materials given, and decide to either Approve, Decline, or Pend, the account requesting more information. This process typically lasts only a day or two, however circumstances may cause this process to take longer.

Getting Started

It will now be up to the processors technical team to do the work. Once the processor has built the file and has deployed the equipment your business will use, you can now begin to accept payment from your customers. To make sure everything is set up correctly, you should run some test transactions to verify you know how to use the system and are receiving deposits. The business owner should also train their staff on proper use of the equipment. Making sure the staff understands how the equipment functions, and how to use it properly. This is something the processors tech support group should be very willing to assist with.

For more information on setting up a merchant account, please email info@merchantequip.com, or by calling (888) 979.6882

Its be long believed by many that PIN debit transaction are cheaper than signature debit and while that may be the case in some instances that is not always the case.

First off a quick clarification, signature debit is when a customer’s debit card is accepted just like a credit card without having the customer enter their PIN number. Conversely, a PIN debit transaction is when the debit card is accepted and the customer enters their PIN as they would do at an ATM machine.

Short answer:

If your ticket size is less than $50, you’re probably better off running a transaction as signature debit. If your ticket is higher than $50 you’re usually better off with PIN debit. The biggest savings as a percentage of the transaction will be on the smaller ticket sales.

For example if you have a $5.00 sale and your PIN debit transaction cost is $0.50 then you’re paying 10%. That same transaction with signature debit could cost you about $0.23 which is more than a 50% savings over the PIN Debit Fee.

But there is a lot more to it than that..

Cost Drivers:

There are 3 primary drivers of cost when talking about debit transactions. The first is going to be whether or not the card being accepted is a regulated or unregulated debit card. The second is which network is being processed through. Finally, the third is the dollar amount being processed. You can look at these three areas to work out a rough idea of your possible costs.

Regulated and Unregulated Cards:

The Durbin amendment set a price cap of effectively 0.05% + $0.21 for cards issued by banks with more than $10 billion in assets. The amendment allows for an additional $0.01 per transaction to be charged in most cases. For issuers under $10 billion in assets there is no regulation as to what they can charge to move funds.

With regulated cards having a $0.22 transaction fee from the network, small tickets are going to have a higher effective cost than unregulated until the transaction amount is above $7.00. For transactions beyond $7.00, regulated debit cost is by far cheaper than unregulated.

Unfortunately, you’re not going to be able to tell what cards are regulated or unregulated. That being the case we are going to focus the rest of this article on unregulated cards where the other two cost drivers come into effect.

Unregulated Network Pricing and Ticket Size:

Each payment network prices transactions differently, however higher dollar transactions will end up with the lower effective cost. No matter if you are accepting PIN or signature debit, if you can increase your per transaction amount, it would be in your best interest from the perspective of effective cost.

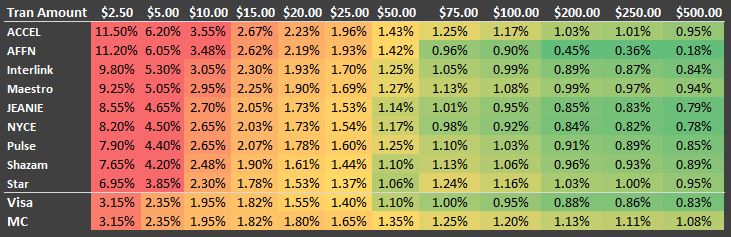

The table below shows a breakdown of the network cost for a single transaction between $2.50 and $500. The first 9 networks represent the effective cost per transaction on PIN Debit. The lower two show the effective cost of processing the same transaction as signature debit.

As you can see, when look at just the network fees, signature debit is effectively the lowest priced option until between $25 and $50 transactions. At $50.00 and higher, the debit networks begin to consistently a cheaper way of accepting the card. With that in mind notice that PIN Debit is at most a savings of 0.30% on a $500 ticket. That’s not a huge savings on one transaction but on a month of volume it can really add up.

The biggest take away here would be for merchants with very small ticket sizes. It would be in their best interest to avoid PIN debit. As a percentage of the transaction amount, signature debit would be their most cost effective option.

Another Important consideration:

Before making changes to how you accept payments just based on your per transaction size, take a look at how much regulated debit you are accepting now. Review your merchant statement or ask your processor about your regulated debit volume.

While you’re at it check and see what your processors is charging you for regulated, and unregulated debit. Make sure to specifically as about signature and PIN debit rates for both transaction types.

You might find that you accept a lot of regulated signature debit, but your pricing on those cards is the same as unregulated, meaning you are not seeing any of the cost savings of those transactions. You might also find that other transaction fees make one transaction type less cost effective that it should be. If this is the case its probably time to re-evaluate your current setup and see what other options are available.

If you have any questions understand a processing statement feel free to reach out to us at 800-898-3436, and we will do breakdown and explanation on any merchant processing statement. You can also email us.

Starting early in 2019, many businesses in the US will lose the ability to force transactions. A forced sales happens when a merchant uses an existing authorization number to push a transaction into the settlement system. While many businesses will never have to do this, it is very common for others. Legitimate reasons for forcing transactions include when sales are processed offline such as a mobile terminal without access to a cellular network, or merchants who still manually imprint cards.

The problem with forcing transactions, is that there is no ability to verify the authorization number before processing the sale. So this is an extremely common method that criminals use to defraud cardholders and processors. They just enter a card number and some random digits for an authorization number and process the card. This has a variety of consequences, but generally ends in the card holder or card issuer requesting a chargeback.

About a year ago, card associations decided they were fed up with the amount of fraud being committed using forced sales so they passed a new regulation requiring processors to disable the ability to force sales for all businesses and only allow it on a case by case basis. This regulation goes into effect in January and will remove the ability to force transactions for most merchants. Some processors are taking it a step further and making it very difficult to force sales even for businesses who have a legitimate need to do so.

So, if you are a business who routinely or occasionally needs to force transactions, be aware that this function is likely to disappear from your terminal, POS system, or payment gateway in January. If you have a legitimate need for it, you will likely be granted access to the function, but it may be literally on a case by case basis.

Colorado’s Online Sales Tax Mess Disaster

While collecting sales tax is a complicated process for ecommerce businesses, Colorado just made it a million times worse by requiring online retailers, both instate and out of state, to collect and remit taxes for sales made in the state of Colorado. Unlike most states who have attempted to make collecting and remitting sales tax easier, Colorado has an extremely complex sales taxation mechanism with dozens of taxation districts and even within these districts the total taxes can be different because Colorado collects taxes based on numerous factors. And to make it even worse, Colorado has a home rule law, where different cities are allowed to control the collection process entirely.

Effective Dec. 1, 2018, the Colorado Department of Revenue will adopt new sales tax rules. The new rules state that sales tax must be collected and remitted based on the jurisdiction’s tax rate at the point of delivery for the taxable good when taxable goods are delivered to a Colorado address outside the retailer’s jurisdiction. This includes any applicable state-administered local and special district taxes. For example, if a retailer delivers taxable goods to a customer’s address, sales tax must now be collected at the rate effective for the customer’s address, not the taxes that are in common between the customer’s address and the seller’s location. For a complete list of location/jurisdiction codes for sales tax filing go here.

So, an out of state online retailer will have to figure out the specific taxation rate depending on the shipping address of the customer at the time of checkout. And, then will have to figure out how to remit those taxes to the state and/or city themself. In other states with consolidated sales tax rates, this isn’t such a problem, but in states like Colorado with complex sales taxation, it is a nightmare for businesses trying to comply with the state’s policies. This is a clear example of putting the cart before the horse and is going to cause serious problems for the few small remaining online retailers who have so far managed to not get put out of business by Amazon.

In our last article we covered how to get your effective rate to better understand what your credit card processing costs vs your processing volume.

Here we are going to take a look at some adjustments that can be made to help lower your effective cost just by making some changes to your operating procedures. With some operational changes you can make an immediate impact on your processing fees. While most business are not going to be able to use all of these methods, even implementing one of the following can do a lot to bring down your effective processing costs.

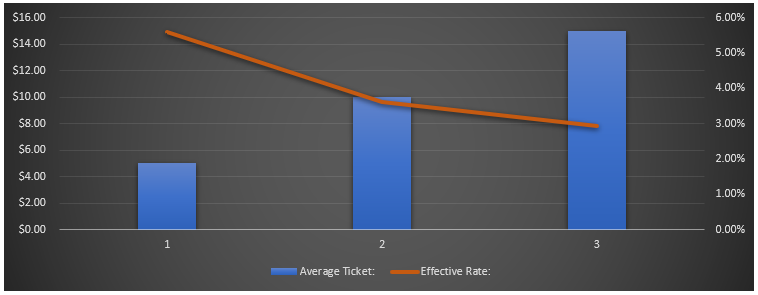

Increasing Ticket Size

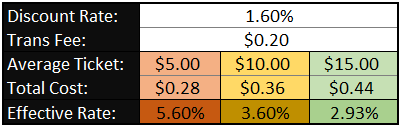

One place to start would be looking at your average ticket size and seeing if increasing it will have a significant effect on your processing statement. The lower your average ticket, the more effect increasing it will have. To understand how this works we should take a look at your processing fees which may be made up of a flat per transaction cost and/or a percentage rate. On lower ticket amounts the transaction fees accounts for a higher percentage of your sale amount than the processing rate.

Here is a quick example of the effect of increasing your ticket size has on your effective rate.

As the average ticket increases the effective rate drops

In this chart you can see how the lower starting average ticket the higher the effect.

Here are a few ways to increase average ticket size.

We are going to list a few of the common ways to increase your average ticket, but don’t be afraid to step outside the box. We have seen many businesses roll out some unique strategies that have done wonders for increasing ticket size.

Bundle Items:

Bundling items will help increase overall sales when done correctly and for our purposes here, bundling will also help push up your average ticket. Quick services restaurants have used combos for years to help increase the amount of food and drinks server. That said it doesn’t just apply to quick service, you can do the same sort of bundling in retail.

While with most retail ticket sizes will be higher you can bundle smaller items to help increase your overall average ticket size.

Add Impulse Items at checkout:

The impulse purchase can be a powerful tool. Adding low cost items at the point of sale can help drive higher tickets. You see this everywhere from the convenience stores and grocery stores to clothing stores and mechanics. Take some time to consider what items would appeal to your specific customers.

Offer Discounts on multiple items:

If you can sell one thing, maybe you can sell two. There is a local automotive repair place in town that offers discounted oil changes if you purchase two or more at a time. In their case, it’s much more about building return customers, but you can do the same while helping to increase ticket sizes.

There is also a favorite donut shop in town that heavily advertises discount for ordering multiple of the same item, allowing them to more efficiently move products and improve their processing costs.

Up Sales and Add-ons

This staple of the fast food industry shouldn’t be overlooked by other business types. Train your staff to know what products or services go together, and to watch for what products are typically purchased together.

Being able to suggest something a customer might be missing from their purchase is just good customer service. Better yet it increases your ticket size.

Gift cards are a great up sale, and way to increase ticket size. They also in-affect accomplish most of the points above in one transaction. They help to build customer loyalty, increase transaction size, increase total customer spend, and generally you are charged a lower flat fee per transaction when compared to standard credit card fees.

Tips can effect your processing rate

All kinds of businesses accept tips, but many don’t realize that it can affect the processing rate charged on a transaction. In the processing industry, only a few business types are routinely acknowledged to accept tips, and even then there are limits. Basically if you’re a restaurant, bar, or saloon, tipped transactions generally won’t increase your discount rate as long as its under 20% of the original sale amount. If your are any other business type tips are essentially not supposed to happen.

And, sometimes tips organically exceed 20% of the original sale amount, and some business allow their employees to receive tips on credit cards. In those instances your processing fees may increase. There are a few things you can do help keep these costs down.

Counter Tip

Counter Tip is a popular alternative to the restaurant normal tip-line on the receipt. With Counter Tip you present a receipt with a tip line before processing the card payment. The card holder can then fill out the tip amount and total and return the receipt with their payment card. When running the transaction you would enter the total payment amount, including the tip, that way the sale is processed with the original authorized amount including the tip. This avoids the transaction costing more due to the tip amount.

Many credit card terminals support this feature out of the box, however some will need to have a configuration update to enable it.

Ask for a tip before finishing the transaction

Similar to counter tip, just asking before processing the sale allows you to enter the total amount entirely avoiding a tip adjustment which can increase your costs.

Cash Tips

Make it known that cash tips are appreciated. The more you move tips to cash, the better. Even when you are getting the best possible rates, you are still paying processing fees to accept a tip. If you are passing those tips directly to your employees then the business is paying fees on money it did not collect.

Proper use of your point of sale

The way you process and handle sales can cause your transaction cost to increase. While this is not an exhaustive list these are the most common things business do that increase their per transaction expenses.

Settling properly

When you run a transaction on your terminal and you receive an approval, no money has moved. Basically at this point the issuer has just reserved those funds for your business. The authorization is only good for a limited period of time and needs to be settled in order for your business to collect those funds.

There are two important time-frames for authorizations. The first is 24 hours from initial authorization. If a transaction is older than 24 hours when it is settled, it can cause the cost to increase. The second time-frame is the expiration of the authorization which depends on the several factors, but general rule of thumb is 7 days. Once an authorization has aged beyond 7 days, not only will the costs increase, but you will also have a higher risk of a dispute by the card holder or the issuer.

Ignoring prompts

When you run a transaction and your terminal prompts for an address or zip code or tax amount, do you ever just leave those blank? If so, it is almost definitely costing additional money.

Conversely, you should take note if your terminal is not prompting for an address or zip code when keying in a transaction. It should be prompting every time you key a sale.

Not all prompts affect the rate charged by issuers and processors however, some do, and it’s important to enter that information not only to keep your rates down, but also to help verify the card holder is who they say they are.

Just a quick heads up, with the address prompt, you only need to enter the numerical portion of the address, not the entire street name, suite, apartment, unit, etc..

Swipe / Chip read everything

You want to be accepting using the chip on every possible card. While not all businesses are going to have physical access to the card but if you can process using the chip, do it, and if you can process by swiping, do it. Not only does this help keep your processing costs down, it is also much more secure. If you accept a stolen card and it was processed using the chip then the card issuer is much more likely to be responsible for liability in case that card is stolen. If you don’t use the chip, then your business is almost always responsible.

Pin Debit?

This is a touchy subject and depends on your average ticket, rates, networks, and location. More and more, debit networks are increasing their pricing and are closing in on or exceeding credit and debit card costs. Also, PIN-Debit may have a higher transactions fees, and now monthly fees, which can end up costing more. Some networks will charge $5 or more dollars per month even if you only accept a single PIN transaction. Further more some PIN-Debit networks will also charge an annual fee if you have accepted one of their card types.

Since the interchange rate on large bank debit cards has cap at $0.05% and $0.22 per transaction it may not bring any savings at all, or it may be more expensive for many merchants.

That said it’s still possible that PIN-debit can save money but it’s very specific to the business and the type and number of PIN transactions they are accepting.

Additional thoughts on lower expenses

For many merchants, more savings can be had by making changes to how they accept card payments, than specifically by lowering rates. It’s important to work with a team that is serious about helping you lower your costs. You should be able to contact your processor and ask them what things you can do to help lower your own costs. If they can’t suggest any improvements for your business and they can’t tell you why then it’s probably time to start seeking a new provider. Your business may be doing everything as efficiently as possible, but they should be able to point this out and explain how what you are doing is the best possible practice for your particular business.

November 4th is right around the corner, don’t forget to update your terminal’s time.

Updating the date and time in the Verifone VX520 terminal can be done quickly using the instructions below. There is also a video below that you can follow along with.

Start on your main sales screen.

Press Enter

Select F2 for Setup

The terminal will prompt for a password. The default password for this device is z66831. This can be entered by pressing 1 followed by the alpha key two times, then entering the remaining digits 66831.

Once on the Setup screen, press the far left purple button to page down until you see Date/Time.

Press the “F” key that corresponds to Date/Time.

The terminal will then prompt for the date. This terminal requires a 4 digit year, so for example Oct 29 2018 would be entered as 10292018.

Press Enter to save and move to the time prompt.

Use 24 hour time to key in your local time. You must enter the seconds, which you usually just set to “00”.

Once the time is entered the terminal will jump back to the setup screen. From there you can press the red “x” key two times to take you back to your main screen.

Here is a video we made if you would like to follow along.

We know how excited you are to receive your credit card processing statement each month. You just can’t wait to open it, stare at it blankly, and finally resign yourself to the comforting feeling of confusion.

Payment processing statements, even simple ones, can seem like hieroglyphics to many, which basically makes them worthless. Even if you understand your processing statement, with all the different fees and details, can you really tell if your getting a deal your happy with?

Let’s cut through all nickels and dimes and get to the heart of what matters, overall cost.

Effective Rate Review:

You don’t need to spend much time at all on any statement to get a feel for what your merchant account costs you. Once you have a basic idea of your payment costs you can go a little deeper, but to start let’s look at getting a baseline. Grab your processing statement, and look for two bits of information.

Your processing volume – To start total up all of the processing volume that your processor deposits into your account. For example if you are funded and billed directly by American Express for your Amex sales, you would not want to include that volume as it doesn’t really apply to the fees.

Your Total fees for the month – Sometimes you will need to add the charges from each section of your processing statement, but most will have the grand total listed. One thing to keep an eye out for is daily discounting. If your processor is debiting your processing fees with each batch you will want to confirm that your statement total includes that amount in its totals. If it does not, you will want to add those daily fees on to your fee total. If you have questions about doing this, just give us a call and we would be happy to lend you a hand.

Now it’s time for some basic math. Your going to divide for total fees by your total volume.

Example

Let’s say you processed $20,000 in volume for the month, and your fees were $589.12.

589.12 / 20,000.00 = 0.029456.

Or as a percentage, 2.95%

So now you have come up with your effective cost, and we can start playing with numbers to see what affects your rate the most.

Fixed Monthly / Annual Fees:

Let’s start with fixed monthly fees. Look at your statement and pick out items that you believe to be fixed monthly and annual fees.

Here are a few examples: Statement / Service Fees, PCI Non Compliance, PCI Annual Fees, Equipment Rentals, etc.

Now subtract those fees from you total processing cost and divide the difference by the total volume. This will give you an effective rate based much more closely to just your processing fees.

Lets remove those monthly fees:

$169.78 – $30 = $139.78

Here we will use the remaining fees to calculate the effective rate again.

$139.78/$5,000 = 0.2796 OR 2.80%

As you can see both of these accounts come up with the same effective rate based on just the processing fees, however their original effective rate that was based on overall cost was quite a bit different. This illustrates how fixed monthly fees skew your effective processing costs on lower volumes.

With these two effective rates, you can see what your entire account is costing you as a percentage of volume, as well as how much of that is just from processing fees.

On the lower volume account it would clearly be more effective to look at lowering your fixed monthly costs. Whereas with the higher volume, it starts to make more sense to focus on processing fee improvements.

Keep in mind that a lot of times processing companies and sales agents will use a general pricing method to simplify the initial understanding. That leaves room for some businesses to receive an effectively better cost than another. You can use this information to help negotiate for pricing that is more effective for your particular business. That said sometimes you can make changes to your business to help improve your effective rate in a much more profound way than just getting your processing costs lowered.

In our next article we are going to look at some ways to lower your effective rate without having to shop around. You may be surprised how much you can effect your processing costs without even calling your processor.

If you missed the previous two parts of Confessions of A Risk Analyst check out part one and part two.

What to do if your funds are on hold?

If you are put on hold, the processor may or may not contact you about it. It generally depends on why you have been put on hold. Most commonly it will be to verify a transaction or batch, in which case it’s customary for the processor to reach out immediately and request invoices, card holder information, and other relevant financial information. It is in your best interest to be courteous and promptly send over what has been asked for. If you cannot provide everything they have asked for just explain what you are able to send and what you can’t send and the reason why. Generally, processors request more than they need to lessen the likelihood they will have to come back and make a second request, so its likely not a problem if you can’t send them everything they ask for right away.

It’s important to be courteous and prompt, and not saying you need to become friends with the risk department, but whether the person you speaking to makes the decisions or is just a liaison for the risk department, these people are part of the process of getting your funds released. Insulting them and telling them your going to cancel will not influence their decision and can often delay any action. Most processors try to handle batch related risk holds the same day in attempt to avoid delay your deposit, so it is in your best interest to respond as quickly as possible. If after you have received your funds you still feel like you don’t like how it was handled, then it would be best to reach out to the processor’s customer support and make a complaint there.

If you notice you are suddenly not receiving batches and the processor has not reached out to you, contact their customer service immediately. Do not mention anything about potentially being on hold, as this just raises suspicions. Most merchants don’t know holds even exist and if you start asking if you’re on hold, it might be assumed that you were doing something you knew could get your funds held. If customer service does find that you are on hold, they will directly you to the proper people to speak with, sometimes it’s just a glitch in the fund transfer system or a minor technical issue. Remember the customer service employees generally don’t have access to detailed information concerning holds and risk related information, so most answers about why, are going to be speculative at best.

Again, once you reach the risk department, go ahead a provide them with whatever they ask for. Risk groups are generally going to ask for invoices, financials, and possibly even tax returns in rare situations. If you feel they are requesting something unreasonable, just talk to them about it. Again, many times they are trying to request more than they need so they don’t have to keep reaching back out to you, if a risk assessor is not satisfied with the initial documentation. If they are looking at your account due to chargeback related issues then the process is definitely going to take longer than a day. In rare and complicated cases, these issues can go on for weeks or month, and the details on those are vary on a case by case basis. This is outside of their control, the issuer controls the chargeback process, the processor is just an advocate for the merchant.

The key takeaway here is that it’s in the processors and the business’s best interest to get risk related issues resolved as quickly as possible. While most risk related issues can be handled within a day, others take more time and energy by both the processor and the business. Remaining professional helps the process move along at its fastest pace. You can always put in a complaint about the process once your funds have been released or if the process has started taking longer than expected.

This will never happen to my business!

You may feel like your business isn’t the type to be victim to fraudulent transactions, customer disputes, or wild changes in transactions or batches and that none of this applies to you.

We’ve worked on dozens of these issues where a business thought it couldn’t happen to them and was crushed by any of the previous mentioned issues. Some of those business knew they were doing something that could get them in trouble, but most were just normal businesses doing what they do and become victims of fraud or a distributor that quit supporting or shipping the products they sold. We’ve had numerous contractors and suppliers who processed very large transactions only to find out later that the transactions were fraudulent. Remember just because you receive an approval authorization, that doesn’t mean the transaction is legitimate indefinitely. A chargeback can be issued in some cases up to 18 months after a transaction was processed and by that time the money has already been spent by the business.

Take time to look at your business and plan for potential risk related issues. Give yourself a sort of pressure test to see where your business is weak and look to avoid deal in those areas or strengthen those areas. Also do research on avoiding card holder fraud. Small changes to your business can a big deterrent for criminals as they tend to only go after easy targets. If you do find yourself in some risk related issues, remain calm and work with the processor to get through it as quickly as possible.

A processor takes a silent backseat to assessing potential risk based on what they know about the business, its owner, and the transaction information. They do this while reserving the right to request additional detailed information about a transaction, the business, the owners, and the company itself. A processor reserves the right to hold funds if they feel the potential risks warrants it. Holding back funds gives them some level of protection against loss but protects the business by not allowing those funds to get spent. If a business obtains those funds and spends them in operating the business, then they could become in debited to the processor who will then end up having to hold back funds to get repaid.

Example: A business was selling custom hot tubs and was successful for the better part of 10 years. The manufacturer they were using changed some of their processes which created a quality issue and caused almost all the products they were selling to stop working shortly after delivery. While the agreement with the manufacturer included a money back guarantee, the process to refund the business was very slow. In the meantime the business was struggling to put a new manufacturer in place to build replacement units not to mention the new orders they had coming in. They were trying to replace and refund every customer. However, with the manufacturing issues, it was taking months to get replacement sent out or refunds processed. These refunds started to turn into chargebacks which immediately began draining the cash reserve the business had on their own. In the meantime, they began accepting new orders and using those funds to refund previous customers, while waiting for their reimbursements and their new products to arrive. After months of struggling to fix their customers issues, everything started to fall apart, they couldn’t float orders anymore, or pay their employees, or deliver whatever products they did end up acquiring.

In the end, the business collapsed leaving the business owner with more than $1.5 million owed back to card holders. The processor ended up covering all of it, and is still in the process of trying to collect from the business owner. Basically because of a change at a supply chain company entirely outside of the oversight of the processor, a thriving business imploded leaving the owner, and subsequently the processor, with millions in debt.

It’s important to have your employees trained to look out for fraud which we cover in a previous articles (link1, link2). Small changes to your business can stop would-be criminals from taking advantage of your business. It’s also important to have backup plans in place to allow your business more flexibility in times of stress. Sometimes just having a line of credit you can draw on to help in a crisis can save a business if used properly. In our next article or two we will cover why processors don’t want to hold funds and what to do if you find yourself with a risk reserve.

Processors don’t want to hold funds!

Truth is, processors don’t want to hold funds. To dispel a common myth, held funds cannot gain interest, so there is no incentive on that part for a processor to place a hold. It is very disruptive to the business, the relationship between the processor and their merchant, and requires a substantial amount of administrative work for everyone. However, holding funds is better than allowing a business to over extend itself and collapse in the worst case scenarios. Most businesses and business owners are not expert risk assessors. They don’t see all the potential pitfalls, and are understandably biased about their invulnerability. A business owner doesn’t understand sometimes that a chargeback can happen at any time and that “big sale” is actually just a chargeback waiting to happen. From time to time this entrepreneurial spirit gets businesses in over their heads and sometimes it’s what causes a business to fail, which is also bad for the processor. Another reason the processor doesn’t want to hold funds is they will have to spend time, money, and resources to internally research and handle these issues. They would rather focus on addressing serious threats and their routine operations. The faster they can get the issue cleared up and funds released, the happier their customers are, and the quicker they can move on to normal operations.

We know how excited you are to receive your credit card processing statement each month. You just can’t wait to open it, stare at it blankly, and finally resign yourself to the comforting feeling of confusion.

We know how excited you are to receive your credit card processing statement each month. You just can’t wait to open it, stare at it blankly, and finally resign yourself to the comforting feeling of confusion. If you are put on hold, the processor may or may not contact you about it. It generally depends on why you have been put on hold. Most commonly it will be to verify a transaction or batch, in which case it’s customary for the processor to reach out immediately and request invoices, card holder information, and other relevant financial information. It is in your best interest to be courteous and promptly send over what has been asked for. If you cannot provide everything they have asked for just explain what you are able to send and what you can’t send and the reason why. Generally, processors request more than they need to lessen the likelihood they will have to come back and make a second request, so its likely not a problem if you can’t send them everything they ask for right away.

If you are put on hold, the processor may or may not contact you about it. It generally depends on why you have been put on hold. Most commonly it will be to verify a transaction or batch, in which case it’s customary for the processor to reach out immediately and request invoices, card holder information, and other relevant financial information. It is in your best interest to be courteous and promptly send over what has been asked for. If you cannot provide everything they have asked for just explain what you are able to send and what you can’t send and the reason why. Generally, processors request more than they need to lessen the likelihood they will have to come back and make a second request, so its likely not a problem if you can’t send them everything they ask for right away. We’ve worked on dozens of these issues where a business thought it couldn’t happen to them and was crushed by any of the previous mentioned issues. Some of those business knew they were doing something that could get them in trouble, but most were just normal businesses doing what they do and become victims of fraud or a distributor that quit supporting or shipping the products they sold. We’ve had numerous contractors and suppliers who processed very large transactions only to find out later that the transactions were fraudulent. Remember just because you receive an approval authorization, that doesn’t mean the transaction is legitimate indefinitely. A chargeback can be issued in some cases up to 18 months after a transaction was processed and by that time the money has already been spent by the business.

We’ve worked on dozens of these issues where a business thought it couldn’t happen to them and was crushed by any of the previous mentioned issues. Some of those business knew they were doing something that could get them in trouble, but most were just normal businesses doing what they do and become victims of fraud or a distributor that quit supporting or shipping the products they sold. We’ve had numerous contractors and suppliers who processed very large transactions only to find out later that the transactions were fraudulent. Remember just because you receive an approval authorization, that doesn’t mean the transaction is legitimate indefinitely. A chargeback can be issued in some cases up to 18 months after a transaction was processed and by that time the money has already been spent by the business. How Processors Assess Risk

How Processors Assess Risk credit you can draw on to help in a crisis can save a business if used properly. In our next article or two we will cover why processors don’t want to hold funds and what to do if you find yourself with a risk reserve.

credit you can draw on to help in a crisis can save a business if used properly. In our next article or two we will cover why processors don’t want to hold funds and what to do if you find yourself with a risk reserve.